France ends Regime 42 in 2026: What EU and non-EU importers need to know.

- Tue, October 07, 2025

- 4.5 Minuten Lesezeit

What is Customs Procedure 42 (Regime 42) and how does it work?

For years, Customs Procedure 42 – also known as Regime 42 – has allowed importers to bring goods into one EU Member State and immediately dispatch them to another EU country without paying import VAT upfront. The VAT was instead reported in the country of destination, making France an attractive entry point for exporters.

For example, a UK company selling goods to a customer in Germany could import the goods into France, clear them under CP42, and transport them directly to Germany. In this case, import VAT would not be paid in France but accounted for in Germany instead.

France ends Customs Procedure 42 (Regime 42) for non-EU importers in 2026

From 1 January 2026, France will abolish this long-standing VAT simplification for non-EU importers, including businesses established in the United Kingdom, Norway, Switzerland and other non-EU jurisdictions.

EU-established businesses are not affected by this change and can continue trading under normal intra-EU VAT rules. However, they may still need a French VAT registration in certain cases (see below).

This reform, introduced under the French Finance Act 2025, aims to tighten VAT control and align France with broader EU anti-fraud measures.

Key French VAT changes for traders taking effect in 2026

Non-EU importers will face new compliance obligations when importing through France:

- Register for French VAT.

- Submit periodic VAT returns declaring import VAT and intra-EU supplies.

- Appoint a fiscal representative (mandatory for non-EU-established businesses).

- Pre-finance import VAT, unless deferred accounting applies through a fiscal representative.

EU businesses may register directly, as a fiscal representative is not required for EU-established businesses, but still have the possibility to make use of fiscal representation.

Regime 42: What really ends – and what remains

There’s been confusion about whether Regime 42 will be abolished entirely. In fact, the procedure itself remains, but the simplified version available to non-EU importers without French VAT registration will end on 1 January 2026.

Myth:

France is abolishing Regime 42 completely.

Fact:

Regime 42 will continue, but non-EU businesses (including those in the UK, Norway and Switzerland) will no longer be able to use the simplified “one-off” model. To keep importing via France, they will need to:

- Register for French VAT;

- Appoint a full fiscal representative; and

- Submit French VAT returns for import VAT and onward EU movements.

For EU-established businesses, Regime 42 remains available under the normal intra-EU VAT rules. The reform mainly removes the exemption that previously benefited non-EU importers.

When and why businesses need to register for French VAT after Regime 42 ends

From 1 January 2026, a French VAT number will be required for:

Non-EU businesses that:

- Import goods into France.

EU businesses that:

- Store goods in France;

- Make domestic supplies in France;

- Take part in a chain transaction involving France.

In addition, French customs may request a VAT number in specific situations to ensure proper VAT control and compliance.

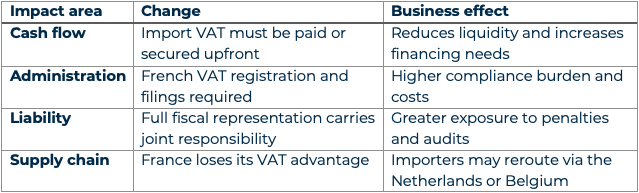

Business impact: what changes for non-EU traders

The withdrawal of Regime 42 will have significant administrative and financial implications for global exporters, particularly for UK, US and Asian businesses currently using France as an import gateway into the EU.

While France may lose some of its competitive edge, importing via France remains possible with the support of a qualified fiscal representative who can manage compliance and cash-flow risks.

Alternative EU import routes offering VAT deferral

With the end of Regime 42, non-EU traders should review other EU entry points that still allow postponed accounting for import VAT. Below are two of the most practical and commonly used solutions for non-EU importers:

The Netherlands – Article 23 licence and fiscal representation (limited/general)

The Dutch Article 23 licence allows importers to declare import VAT on their VAT return instead of paying it upfront. This provides a major cash-flow advantage and simplifies administration, keeping the Netherlands a preferred EU import hub.

Belgium – ET 14000 authorisation and fiscal representation (global/individual)

Under Belgium’s ET 14000 scheme, import VAT can be postponed and accounted for through the VAT return, provided the importer meets Belgian compliance requirements. This makes Belgium another flexible alternative for non-EU businesses.

Both countries remain strategically advantageous for businesses seeking efficient, compliant import routes once France withdraws Regime 42.

Five steps to prepare for France’s 2026 VAT reform

Here are five practical steps we recommend you take to prepare for the end of Regime 42 and ensure your imports into the EU remain compliant and cost-efficient. Non-EU businesses should begin planning their response to France’s VAT reform well in advance of 2026.

- Review your current import routes – Identify where Regime 42 is currently used and calculate the potential cash-flow impact once upfront VAT payments apply.

- Compare alternative EU ports – Evaluate the Netherlands, Belgium or Germany for logistics efficiency, VAT deferral options and overall cost benefits.

- Register for French VAT early – If you plan to continue using France as your entry point, start the registration process as soon as possible to avoid delays.

- Reassess your Incoterms – Consider moving from DDP (Delivered Duty Paid) to DAP or EXW, reducing your exposure to French VAT obligations.

- Work with a trusted fiscal representative – Choose a partner experienced in managing VAT compliance and representation.

Early preparation will help businesses avoid customs delays, financial penalties and unnecessary administrative costs once the new regime takes effect.

Why proactive action is essential

The end of Regime 42 marks a structural shift in EU import procedures. Businesses that act early can minimise disruption and preserve cash-flow efficiency, while those that delay may face blocked imports, financial strain, and loss of competitiveness.

Businesses using France as a logistics hub should reassess their VAT and customs strategy now, considering how best to maintain smooth EU access after 2026.

How Gaston Schul helps businesses prepare for France’s 2026 VAT reform

We help businesses navigate the upcoming VAT changes through registration, fiscal representation, customs clearance and end-to-end import solutions across Europe. Our experts:

- Register businesses for French VAT and ensure full compliance with the new requirements, including the submission of periodic VAT returns.

- Manage customs clearance procedures and coordinate with local authorities to ensure goods enter the EU smoothly and compliantly.

- Assess and implement alternative import routes through the Netherlands or Belgium to improve cash flow and efficiency.

- Restructure supply chains to stay compliant and avoid operational disruption.

- Analyse and minimise cash-flow impact caused by the end of Regime 42.

If your business is based in the United Kingdom, Norway, Switzerland or elsewhere outside the EU and currently imports via France, now is the time to act.

Contact us today to stay compliant, protect liquidity and ensure a smooth transition ahead of France’s 2026 VAT reform.

Ready to adapt your import strategy before France ends Regime 42?

Complete the form on the right to connect with our VAT and customs experts. Get a tailored solution for your business – from VAT registration and fiscal representation to designing efficient import routes within the EU.

Stay ahead of the 2026 VAT reform – protect your cash flow, avoid compliance risks and keep your EU trade running smoothly.

Partner with us for practical, end-to-end support and take the next step towards a smarter, more resilient VAT and customs strategy today.

Verwandte Nachrichten und Artikel

Erhalten Sie unsere Expertenmeinungen und Zollinformationen direkt in Ihren Posteingang

Mit Ihrer Anmeldung erklären Sie sich damit einverstanden, dass Gaston Schul Sie über unsere relevanten Inhalte, Produkte und Veranstaltungen informiert. Sie können sich jederzeit abmelden. Weitere Informationen finden Sie in unserer Datenschutzrichtlinie.